In this Article

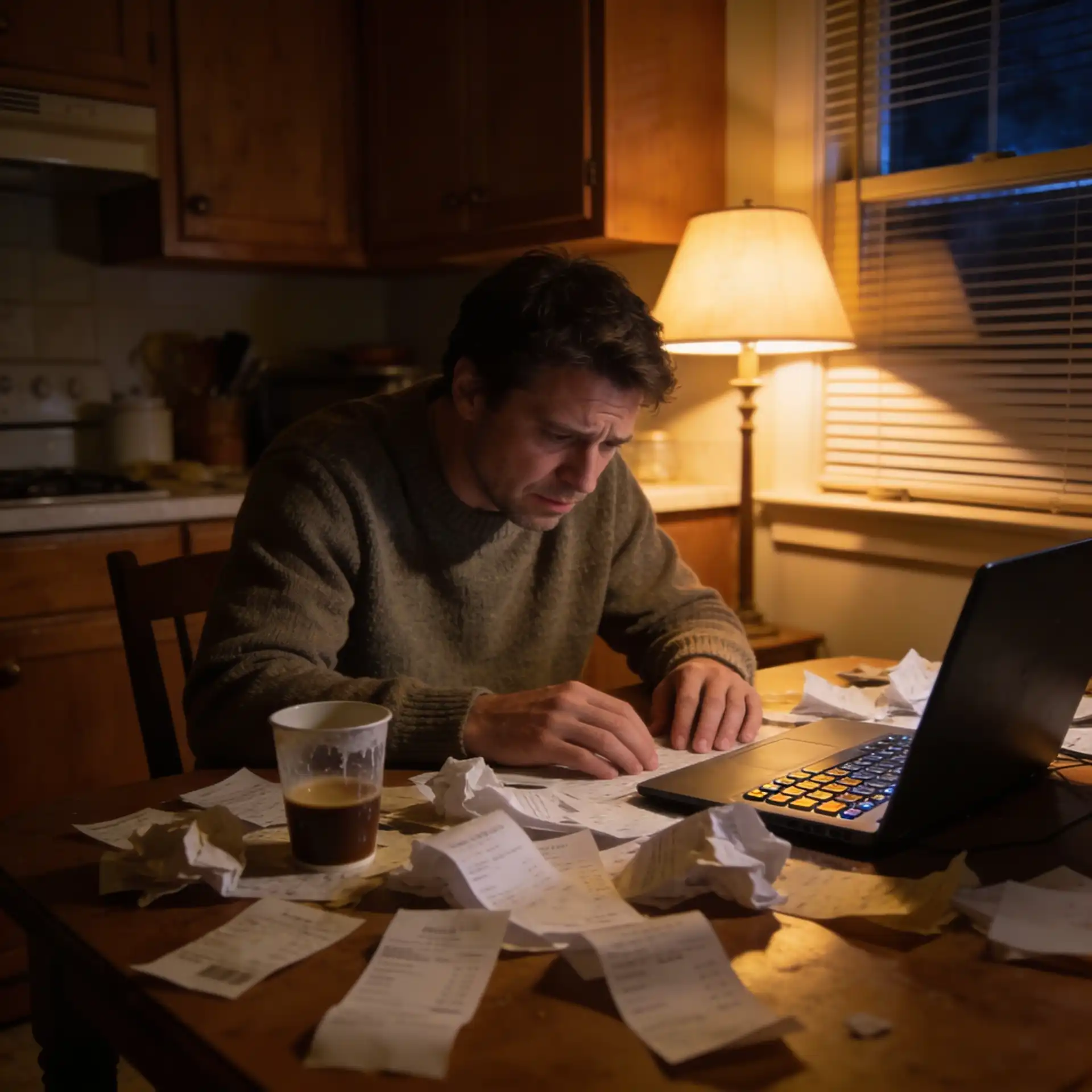

It’s 11 p.m. on a Tuesday in April. You’re at the kitchen table somewhere off the NJ Parkway, staring at a shoebox of crumpled receipts and a QuickBooks file you haven’t opened since November. Your accountant needs everything by Friday. You have no idea what your business made last quarter.

If that hit close to home, you’re not alone. Most New Jersey small business owners we’ve worked with came to us after months, sometimes years, of pushing bookkeeping to the bottom of the list. And every single one of them learned the same thing the hard way: the consequences of not doing your books aren’t theoretical. They’re financial, legal, and personal. And, they get worse the longer you let them sit.

Here’s what actually happens.

9 Real Consequences for NJ Small Business Owners Who Skip Their Books

1. The IRS and NJ Division of Taxation Don’t Forget. They Just Add Penalties.

New Jersey small businesses operate under one of the more aggressive tax regimes in the country.

Here’s what you’re up against before sales tax even enters the picture:

- Federal income tax – your baseline obligation to the IRS

- NJ state income tax – a second layer from the NJ Division of Taxation

- Corporation Business Tax – applies if you’re a C-Corp or certain LLC structures

- Quarterly estimated payments – due four times a year, to both the IRS and the state

That’s four separate tax obligations running simultaneously, and sales tax is still waiting in the wings.

When your books aren’t updated, you can’t accurately calculate what you owe. That leads to underpayment, which leads to penalties and interest added to the original bill. The IRS failure-to-pay penalty runs 0.5% of unpaid taxes per month. New Jersey adds its own late-payment penalties and interest on top. Six months of ignored books can easily turn a $5,000.00 tax bill into $7,000.00 or more.

NJ Business Owner Alert: New Jersey requires all LLCs and corporations to file an annual report with a $75.00 fee, separate from your tax obligations. Corporations and LLCs taxed as corporations also owe a CBT minimum tax starting at $500.00, while multi-member LLCs taxed as partnerships owe a $150.00 minimum partner tax. Ignore these long enough, and NJ can revoke your good standing or administratively dissolve your entity.

2. You’ll Almost Certainly Overpay Your Taxes

This one stings the most, honestly. Without organized books, you can’t track deductions properly. Every untracked expense is a deduction you’re handing back to the IRS. Here’s what gets missed:

- Mileage — every trip to a job site in Bergen County adds up fast

- Software subscriptions — the tools keeping your business running are deductible

- Home office expenses — a legitimate write-off that most small business owners underuse

- Contractor payments — miss these and you’re overstating your net income

- Business meals — deductible (at 50%), but only if you logged them

- Professional development — courses, certifications, conferences all count

- Equipment depreciation — often one of the largest deductions on the table

Without organized books, none of these make it onto your return. That’s not a tax problem, that’s a recordkeeping problem with a tax consequence.

We’ve seen NJ business owners overpay by $4,000.00 to $15,000.00 a year simply because their books were too messy to support legitimate deductions. Your accountant can only work with what you give them.

3. Your Cash Flow Becomes a Guessing Game

Profit isn’t cash. We’ve watched profitable NJ businesses run out of money because the owner had no idea when invoices were due, what was still outstanding, or how much was sitting in receivables versus the actual bank account.

When your books are current, you can answer three questions in under five minutes: How much cash do I actually have right now? Who owes me money, and when? What bills are coming in the next 30 days?

Without a system, those questions take days to answer, if you can answer them at all. That’s how good businesses miss payroll, bounce vendor checks, or take on debt they don’t actually need.

4. Your LLC or S-Corp Status Could Be at Risk

Most owners don’t see this one coming. New Jersey LLCs and S-Corps receive their liability protection in part because they operate as legally separate entities. This means their finances are distinct from the owners’.

When your books are a mess, and you’ve been mixing personal and business expenses, you chip away at what’s called the “corporate veil.” If you face a lawsuit, a plaintiff’s attorney can argue your business isn’t truly separate from you. This puts your personal assets, your house, and your savings at risk of being seized in a judgment. Clean, separate books are one of the cheapest forms of liability protection you can buy.

5. You Can’t Get a Business Loan, Line of Credit, or SBA Funding

Walk into any NJ community bank or apply for an SBA loan, and the first thing they’ll ask for is two to three years of clean financial statements. Profit and loss. Balance sheet. Tax returns that match your books.

If you can’t produce those, the conversation ends. We’ve watched NJ business owners lose equipment financing, expansion capital, and emergency credit lines because their books couldn’t tell a coherent story. By the time they finally cleaned things up, the window had closed.

6. An Audit Becomes a Nightmare Instead of an Inconvenience

Audits happen. The IRS audits a small percentage of small business returns every year, and the NJ Division of Taxation runs its own program. Sales tax audits are especially common for retail, restaurants, and service businesses across the state.

If your records are organized, an audit is manageable but still annoying. Your accountant produces the documentation, you answer the questions, and you move on.

If your books are a mess, it becomes a months-long ordeal. Every undocumented expense gets disallowed. Every cash deposit you can’t explain gets treated as taxable income. We’ve seen businesses in NJ get hit with five-figure assessments for amounts they didn’t actually owe; they just couldn’t prove it.

Pro tip: The NJ Division of Taxation (which has a sales tax rate of 6.625%) can audit sales tax returns for up to 4 years. If you haven’t been reconciling sales to your point-of-sale system monthly, start now.

7. You Can’t Sell Your Business When You’re Ready

Maybe you’re not thinking about selling yet. Most NJ business owners we work with are not doing it, until suddenly they are. A health issue, a partnership dispute, a good offer, or retirement arriving faster than expected.

When that day comes, the first thing any serious buyer or broker asks for is three years of clean financials. Buyers price businesses on documented, verifiable cash flow. If your books are unreliable, your business is worth a fraction of what it should be, or it’s not sellable at all.

We’ve seen NJ business owners walk away from six-figure offers because their books couldn’t support the asking price. It’s completely preventable.

8. The Emotional Toll Is Real

This one doesn’t show up on a Profit and Loss statement, but it shows up everywhere else. The low-grade anxiety that never fully goes away. Avoiding your inbox because you don’t want to see another invoice follow-up. Lying awake, wondering about payroll. The shame every time someone asks how the business is doing, and you don’t really know.

Business owners we’ve worked with describe it the same way: a weight they didn’t know they were carrying until it was gone. Clean books don’t just give you data; they give you peace of mind.

9. It Costs Two to Five Times More to Fix Than to Maintain

Monthly bookkeeping for a small business in NJ typically costs $300.00 to $800.00, depending on transaction volume and complexity. That’s $3,600.00 to $9,600.00 a year for clean, current, tax-ready books.

Catch-up bookkeeping, going back 12, 24, or 36 months and rebuilding everything, typically runs $1,500.00 to $8,000.00 or more as a one-time project, on top of whatever penalties and overpaid taxes you’ve already incurred. The longer you wait, the more it costs, because more transactions need to be reconstructed and more documentation has been lost. Maintaining is always cheaper than rebuilding. Always.

What to Do If You’re Already Behind

If you recognized your business in five or more of those points, you’re not stuck. But you do need to act. Here’s the order we recommend:

- Stop the bleeding first. Get a system in place and start categorizing transactions from today forward. Don’t try to fix the past until the present is under control.

- Get a catch-up assessment. A qualified NJ bookkeeper can review your accounts, tell you how far behind you are, and quote a realistic catch-up project. This usually takes 30 to 60 minutes and should be free.

- Prioritize tax filings. If you’re behind on federal or NJ state filings, work with an accountant to file extensions or get current before penalties keep stacking.

- Build a monthly rhythm. Once you’re current, your monthly reconciliation and reporting keep you out of the crisis cycle for good.

Conclusion

Not doing your books in New Jersey doesn’t just mean a rough April. It means overpaying taxes, missing deductions, weakening your liability protection, losing access to financing, and carrying the kind of low-grade dread that follows you home every night. The fix is straightforward. The sooner you start, the cheaper and easier it gets. If your books are behind, messy, or nonexistent. The Chamberlain Accounting Firm provides comprehensive bookkeeping solutions, including individual tax returns (1040) and business returns (1065, 1120, 1120S). We also specialize in law firm accounting. We proudly serve clients throughout Bergen County, New Jersey, and nearby communities, as well as multiple states across the U.S. For personalized guidance and reliable support, reach out to us online or call (201) 371-3344 today.

Frequently Asked Questions

The NJ Division of Taxation can audit sales tax returns for up to four years. If your records aren't reconciled during that window, undocumented expenses can be disallowed and unexplained deposits may be treated as taxable income.

Catch-up bookkeeping typically runs $1,500 to $8,000 or more as a one-time project, depending on how many months need to be reconstructed. This is on top of any penalties already incurred, which is why starting sooner always costs less

Yes. In New Jersey, LLCs and S-Corps offer liability protection only when business and personal finances are clearly separate. Commingled or disorganized records can weaken the "corporate veil," potentially exposing your personal savings or property in a lawsuit.

Disclaimer: This article is provided for general informational purposes only and does not constitute accounting, tax, or financial advice. The information contained herein is not intended to be relied upon for specific tax, accounting, or financial decisions, and may not reflect current tax law or guidance. No opinion expressed herein may be used for the purpose of avoiding penalties under federal, state, or local tax laws. Readers should consult with a qualified accounting or tax professional regarding their specific circumstances. This communication does not create an accountant-client or advisory relationship.