In this Article

The U.S. doesn’t tax your entire income at one rate; it slices it into layers, each taxed differently. Understanding this simple truth changes everything about how you read your paycheck.

Every April, millions of Americans confront a system they were never quite taught to understand. The federal income tax operates on a principle that is more elegant than most people realize: the progressive bracket system. Rather than applying a single flat rate to everything you earn, the IRS divides your taxable income into ranges, which are called brackets, and taxes each range at its own rate.

How the U.S. Tax System Works

The result of the progressive system is elegant. Which means that if you earn more money, you always have more. The highest dollar of your income is taxed differently from the first. The misconception that a raise could push you into a higher bracket and leave you with less take-home pay is simply false; only the dollars above the threshold are subject to the higher rate.

This distinction is perhaps the single most important concept in personal tax literacy. Millions of taxpayers misread their situation by conflating their marginal bracket with their actual tax burden. They are not the same thing, and understanding the difference is foundational to every tax decision you will ever make.

2025 Federal Income Tax Brackets

For the 2025 tax year, the IRS maintains seven marginal rates. Use the tabs below to view brackets for single filers and married couples filing jointly.

Single Filer

| Rate | Taxable Income Range | Tax Owed |

| 10% | $0 – $11,925 | 10% of taxable income |

| 12% | $11,926 – $48,475 | $1,193 + 12% over $11,925 |

| 22% | $48,476 – $103,350 | $5,579 + 22% over $48,475 |

| 24% | $103,351 – $197,300 | $17,651 + 24% over $103,350 |

| 32% | $197,301 – $250,525 | $40,199 + 32% over $197,300 |

| 35% | $250,526 – $626,350 | $57,231 + 35% over $250,525 |

| 37% | Over $626,350 | $188,770 + 37% over $626,350 |

Married Filing Jointly

| Rate | Taxable Income Range | Tax Owed |

| 10% | $0 – $23,850 | 10% of taxable income |

| 12% | $23,851 – $96,950 | $2,385 + 12% over $23,850 |

| 22% | $96,951 – $206,700 | $11,157 + 22% over $96,950 |

| 24% | $206,701 – $394,600 | $35,302 + 24% over $206,700 |

| 32% | $394,601 – $501,050 | $80,398 + 32% over $394,600 |

| 35% | $501,051 – $751,600 | $114,462 + 35% over $501,050 |

| 37% | Over $751,601 | $202,154 + 37% over $751,601 |

Married Filing Separately

| Rate | Taxable Income Range | Tax Owed |

| 10% | $0 – $11,925 | 10% of taxable income |

| 12% | $11,926 – $48,475 | $1,192.50 + 12% of the amount over $11,925 |

| 22% | $48,476 – $103,350 | $5,579.50 + 22% of the amount over $48,475 |

| 24% | $103,351 – $197,300 | $17,651.00 + 24% of the amount over $103,350 |

| 32% | $197,301 – $250,525 | $40,199.00 + 32% of the amount over $197,300 |

| 35% | $250,526 – $375,800 | $57,231.00 + 35% of the amount over $250,525 |

| 37% | Over $375,801 | $101,077.25 + 37% of the amount over $375,800 |

Head of household

| Rate | Taxable Income Range | Tax Owed |

| 10% | $0 – $17,000 | 10% of taxable income |

| 12% | $17,001 – $64,850 | $1,700 + 12% over $17,000 |

| 22% | $64,851 – $103,350 | $7,442 + 22% over $64,850 |

| 24% | $103,351 – $197,300 | $15,912 + 24% over $103,350 |

| 32% | $197,301– $250,500 | $38,460 + 32% over $197,300 |

| 35% | $250,501 – $626,350 | $55,484 + 35% over $250,500 |

| 37% | Over $626,351 | $187,031.50 + 37% over $626,350 |

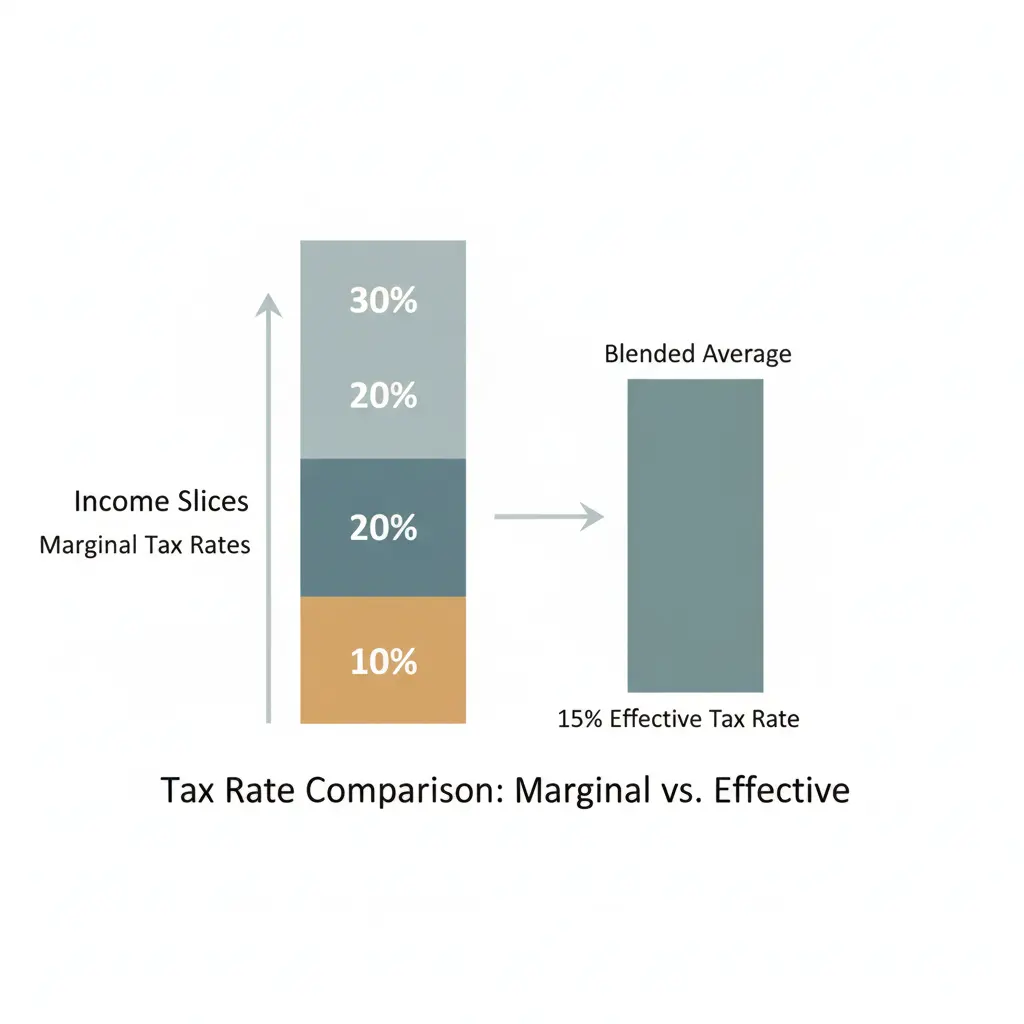

Marginal vs. Effective Tax Rate

This distinction trips up most taxpayers. Your marginal tax rate is the rate applied to your last dollar of income in the bracket you fall into. Your effective tax rate is the actual percentage of your total income paid in tax. That means it’s always lower than your marginal rate.

Example:

Imagine a single filer with $80,000 in taxable income. Individuals in the 22% tax bracket do not pay 22% on the full $80,000 of their income. They pay 10% on the first $11,925, 12% on the next $36,550, 22% only on the remaining $31,525.

Their total federal tax is roughly $13,000, an effective rate of about 16%, not 22%.

Standard Deduction: What Actually Gets Taxed

You do not pay taxes on your gross income. First, the IRS allows you to subtract a standard deduction. You can also itemize deductions if they exceed the standard deduction to arrive at your taxable income.

For 2025, the standard deduction is $15,750 for single filers, $31,500 for married couples filing jointly, $15,750 for married filing separately, and $23,625 for head of Household. That means a single person earning $60,000 would have only $44,250 in taxable income before any other adjustments.

How Taxable Income Is Determined

To determine your tax bill from your paycheck, follow these three sequential adjustments: first, reduce your gross income by the above-the-line deductions to calculate your AGI. Next, subtract the standard (or itemized) deduction from your AGI to find your taxable income. Finally, apply the bracket table to your taxable income. Tax credits are then applied to reduce the resulting bill directly.

- Gross Income: All income before any deductions, which includes wages, freelance earnings, dividends, rental income, and more.

- Adjusted Gross Income (AGI): Gross income minus above-the-line deductions such as IRA contributions, student loan interest, and health savings account contributions.

- Taxable Income: AGI minus the standard or itemized deduction. This is the number that the brackets are actually applied to.

- Tax Credits: Dollar-for-dollar reductions in the tax you owe, applied after brackets are calculated. More powerful than deductions of equivalent size.

A Separate Tax System for Investment Income

Investment income is the profits from selling stocks, real estate, or other assets. That is taxed under a separate, preferential rate schedule. The treatment depends entirely on how long you held the asset.

Long-Term Gains: Held over 12 months

Preferential rates based on total taxable income. Most middle-income earners, roughly $49,450 to $545,500 for single filers, which is qualify for the 0% to 20% rate on taxable income thresholds. High earners may also owe the 3.8% Net Investment Income Tax.

Short-Term Gains: Held 12 months or less

Taxed exactly like regular income, at your marginal bracket rate. No preferential treatment. Holding an asset for more than 1 year can yield significant tax savings.

Withholding and the April Filing Deadline

For most wage earners, employers withhold federal income tax throughout the year. It is a pay-as-you-go system established to ensure consistent government revenue. When you file a return each spring, you reconcile what was withheld against what you actually owe.

Jan – Dec: Employer Withholding

Each paycheck, your employer withholds an estimated portion of your tax based on the W-4 form you filed. These payments are remitted directly to the IRS on your behalf.

January 31: W-2 and 1099 Deadline

Employers and other payers must furnish income statements. These documents summarize the income paid and taxes withheld during the prior year.

April 15: Return Filing Deadline

You reconcile the year. An overpayment results in a refund; an underpayment means you owe the difference, sometimes with a penalty for insufficient withholding.

Quarterly: Estimated Payments (Self-Employed)

Self-employed individuals and those with significant non-wage income, such as dividends, rental income, and freelance earnings, must make quarterly estimated tax payments directly to the IRS to avoid underpayment penalties.

Conclusion

In the end, understanding how the federal tax system works gives you a clear advantage. It’s built to be progressive, meaning higher earners pay more based on their higher incomes, while everyone benefits from lower rates on their first income. But what truly matters isn’t just your marginal bracket; it’s your effective rate, the deductions that reduce your taxable income, and the specific rules that apply to different types of earnings.

When you see the full picture, how marginal and effective rates differ, how deductions shape your taxable base, and how income is categorized and taxed, you move from guesswork to strategy. That’s where real tax planning begins: not avoiding taxes, but understanding exactly how each additional dollar is treated and making informed decisions around it. Tax rules are complex, and the cost of a mistake often exceeds the cost of professional help. The Chamberlain Accounting Firm offers a full suite of services, which includes individual returns (1040), business filings (1065, 1120, 1120S), bookkeeping, and specialized support for law firms. Serving clients across Bergen County, New Jersey, and multiple states nationwide. To get started, contact us online or call (201) 371-3344.

Frequently Asked Questions

No. Only the dollars above the new bracket threshold are taxed at the higher rate, and your previous income is unaffected.

Your marginal rate applies only to your last dollar of income. Your effective rate is the actual percentage of your total income that is paid in taxes, which is always lower.

Not always. Long-term gains (assets held for more than 12 months) qualify for preferential rates of 0%, 15%, or 20%, depending on your taxable income, which are significantly lower than ordinary income tax rates.

Disclaimer: This article is provided for general informational purposes only and does not constitute accounting, tax, or financial advice. The information contained herein is not intended to be relied upon for specific tax, accounting, or financial decisions, and may not reflect current tax law or guidance. No opinion expressed herein may be used for the purpose of avoiding penalties under federal, state, or local tax laws. Readers should consult with a qualified accounting or tax professional regarding their specific circumstances. This communication does not create an accountant-client or advisory relationship.