In this Article

There’s a moment, maybe it’s watching your parent struggle with stairs, or hearing them mention a doctor’s visit, when it hits you: we haven’t talked about any of this. No discussion of accounts. No idea where the will is. No clue what they’d want if a health crisis strikes.

That realization is uncomfortable, but it’s also a gift, because it means you still have time. Preparing for a parent’s death financially isn’t morbid. It’s one of the most loving things you can do for your family. It protects them, and it protects you.

Here’s a walkthrough of the practical financial steps to take now, while the conversations are still possible and the documents are still within reach.

Start the Conversation Before It Becomes Urgent

Most families avoid this topic entirely until a health crisis forces it at the worst possible time.

Bringing up money and end-of-life planning can feel awkward, even disrespectful. But families who have this conversation early almost always say they’re grateful they did. Those who don’t often spend months after a parent’s death untangling confusion, conflict, and legal complications.

A gentle way to open the door: “I’ve been thinking about getting my own documents in order. Would you be willing to walk me through yours sometime?” That frames it as a mutual exercise rather than a conversation about their mortality.

When you do sit down together, try to cover:

- Where their important financial documents are stored

- Whether they have a will or trust, and when it was last updated

- What bank, investment, and retirement accounts exist

- Whether they have life insurance and who the beneficiaries are

- Any outstanding debts or recurring obligations

- Their wishes for end-of-life care and funeral arrangements

You don’t have to cover all of it at once. A few calm conversations over time beat one overwhelming “estate planning talk.”

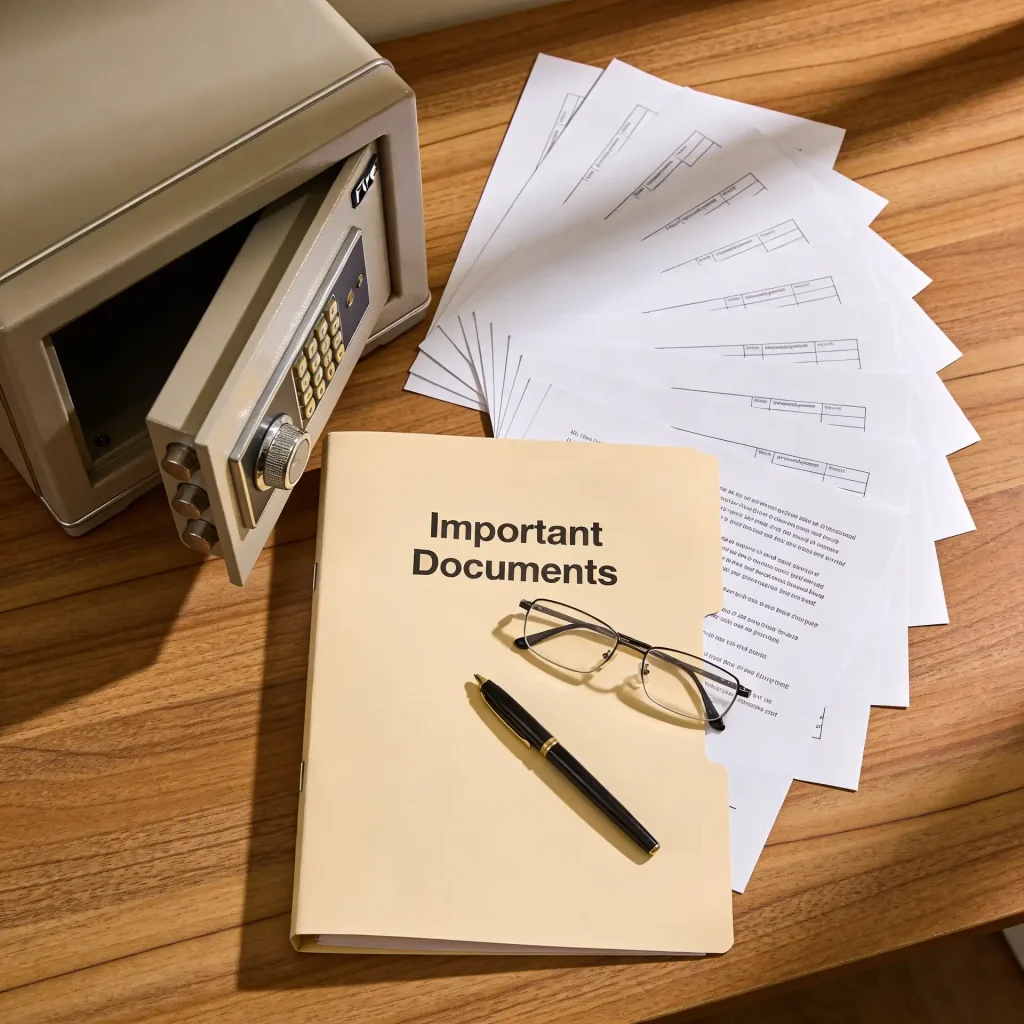

Gather and Organize Key Financial Documents

Once the conversation is open, work together to locate and organize what will matter most.

The core documents to find:

- Will or living trust — the foundation of their estate plan

- Durable power of attorney — grants you authority to manage finances if they become incapacitated

- Advance Healthcare Directives — separate from financial POA; covers medical decisions

- Life insurance policies — including policy number, insurer, and named beneficiaries

- Bank and investment account statements — including online login access, or at a minimum, account numbers

- Retirement account information — 401(k), IRA, pension details

- Property deeds

- Vehicle titles

- A list of recurring bills

Store originals somewhere secure; a fireproof safe is ideal. Make sure at least one trusted family member knows where everything is.

💡 Pro Tip: The document most families forget is the durable power of attorney. Without it, if your parent becomes incapacitated before they die, you may need a costly court process called guardianship or conservatorship just to manage their basic finances. Get this done while they’re still legally able to sign.

Understand What Happens to Their Money When They Die

A common assumption is that a will controls everything. It doesn’t, and misunderstanding this causes real problems.

The key distinction is probate vs. non-probate assets:

Non-probate assets pass directly to beneficiaries, entirely outside the will. Life insurance proceeds, retirement accounts, jointly held bank accounts, and accounts with a named payable-on-death (POD) beneficiary all fall into this category. They transfer quickly and privately.

Probate assets go through a court-supervised process, either under the will or under state law if there isn’t one.

⚠️ Watch Out: Beneficiary designations on retirement accounts and life insurance override whatever the will says. If your parent named an ex-spouse as beneficiary on an old IRA and never updated it, that ex-spouse gets the money, regardless of what the will states. Review beneficiary designations now and update them if needed.

If your parent dies without a will (called dying “intestate”), state law determines who inherits what. In most states, that defaults to a spouse first, then children, but the process is slower and offers no flexibility.

Plan for the Costs You May Not Expect

Even when a parent has savings, the costs surrounding death can catch families off guard.

Funeral and burial costs average between $8,000 and $12,000 in the United States, depending on the choices made. Cremation runs significantly less, typically $1,500 to $3,500. If your parent has strong preferences, document them. Pre-paying for funeral arrangements is something many families find genuinely useful.

End-of-life medical care is often the largest expense. A semi-private room in a nursing home costs over $90,000 per year on average. Medicare covers limited skilled nursing care; Medicaid covers long-term care only after assets are largely spent down. If your parent has long-term care insurance, find that policy now.

Estate administration costs include probate court fees, executor fees, and attorney fees. A properly structured trust can minimize or eliminate probate costs, though there are reasons not to get a trust that can outweigh that benefit.

A few tax things worth knowing:

- The federal estate tax only applies to estates over $15 million (the 2026 threshold), so most families won’t be affected.

- Inherited IRAs come with specific withdrawal rules. Non-spouse beneficiaries generally must withdraw all funds within 10 years. Mishandling this triggers unnecessary taxes.

- Assets inherited at death typically receive a stepped-up cost basis, which can reduce capital gains taxes if you sell inherited property or investments.

Protect Yourself Financially Too

Preparing for a parent’s death isn’t only about their finances. Your own financial stability is at stake.

Don’t co-sign debt you can’t absorb. Children aren’t automatically responsible for a parent’s debts, but if you co-signed a loan, you are. Review any joint financial obligations carefully.

Plan for time off work. Caregiving often intensifies in the final months. Talk to your employer about FMLA rights, which provide up to 12 weeks of unpaid, job-protected leave for qualifying family situations. If you’re self-employed, plan your cash flow accordingly.

Address sibling dynamics early. Money and grief are a difficult combination. Unequal inheritances, old loans that some kids received and others didn’t, disagreements about caregiving responsibilities, these tensions will surface. A direct, calm conversation with siblings before your parent dies, rather than after, reduces conflict far more than any legal document can.

Work With the Right Professionals

Some of this you can research and manage on your own. Other parts genuinely need expert guidance.

- Estate planning attorney — useful for reviewing estate documents, handling complex estates, tax issues, family conflict, real property, and much more. Even a simple will is usually worth the cost.

- Certified Financial Planner (CFP) — can help review retirement accounts, beneficiary designations, and overall estate structure.

- Accountant — important for estates with significant assets, inherited retirement accounts, property that may be sold, and anything involving income taxes.

- Geriatric care manager — not a financial professional, but invaluable for coordinating care decisions and advising on costs, which carry major financial implications.

For straightforward situations, a small estate with clear beneficiaries and no disputes, you may need minimal outside help. But if there’s a family business, multiple properties, a blended family, or substantial assets, professional guidance pays for itself many times over.

You’re Already Doing the Right Thing

This work isn’t easy. It requires sitting with something most of us would rather not think about. But the families who do it ahead of time, who have the conversations, find the documents, and understand the plan, are the ones who can grieve fully when the time comes, without financial chaos piled on top.

Start small. This week, have one conversation. Ask where the will is. Find out if a power of attorney exists. That single step is more than most families ever take. The most important thing you can give your parent right now isn’t money. It’s a plan. The Chamberlain Accounting Firm provides comprehensive bookkeeping solutions, including individual tax returns (1040) and business returns (1065, 1120, 1120S). We also specialize in law firm accounting. We proudly serve clients throughout Bergen County, New Jersey, and nearby communities, as well as multiple states across the U.S. For personalized guidance and reliable support, reach out to us online or call (201) 371-3344 today.

Frequently Asked Questions

The most critical documents include a will or living trust, durable power of attorney, advance healthcare directives, life insurance policies, bank and retirement account statements, property deeds, and a list of recurring bills. Store originals in a fireproof safe and ensure a trusted family member knows where they are.

No. Assets like retirement accounts, life insurance, and jointly held bank accounts pass directly to named beneficiaries — completely outside the will. Outdated beneficiary designations can override your parent's current wishes, so it's important to review and update them regularly.

Generally, children are not automatically responsible for a deceased parent's debts. However, if you co-signed any loans or are a joint account holder, you may be liable for those specific obligations. Always review any shared financial arrangements carefully before and after a parent's passing.

Disclaimer: This article is provided for general informational purposes only and does not constitute accounting, tax, or financial advice. The information contained herein is not intended to be relied upon for specific tax, accounting, or financial decisions, and may not reflect current tax law or guidance. No opinion expressed herein may be used for the purpose of avoiding penalties under federal, state, or local tax laws. Readers should consult with a qualified accounting or tax professional regarding their specific circumstances. This communication does not create an accountant-client or advisory relationship.