In this Article

From state income tax to city surcharges and property levies, New York’s tax landscape is one of the most complex and costliest in the country. It is consistently ranked among the highest-taxed states in the United States. Residents face a layered system of taxes that includes a progressive state income tax, a city income tax if you live in New York City, a federal income tax, and various sales, property, and estate taxes. Understanding how each layer works and how they interact can mean the difference between overpaying and keeping more of what you earn.

New York Tax Rates at a Glance

| Tax | Rate |

| Top state income tax rate | 10.9% |

| NYC additional city tax | 3.876% |

| Statewide sales tax | 4% |

| NYC combined sales tax | 8.875% |

New York State Income Tax

New York uses a progressive income tax system. It means your rate increases as your income rises. Crucially, only the income within each bracket is taxed at that bracket’s rate and not your entire income.

2025 Tax Brackets

There are nine tax brackets for 2025, ranging from 4% at the lowest level to 10.9% at the very top.

| Filing status (single) | Income range | Tax rate |

| Bracket 1 | $0 – $17,150 | 4.00% |

| Bracket 2 | $17,151 – $23,600 | 4.50% |

| Bracket 3 | $23,601 – $27,900 | 5.25% |

| Bracket 4 | $27,901 – $161,550 | 5.85% |

| Bracket 5 | $161,551 – $323,200 | 6.25% |

| Bracket 6 | $323,201 – $2,155,350 | 6.85% |

| Bracket 7 | $2,155,351 – $5,000,000 | 9.65% |

| Bracket 8 | $5,000,001 – $25,000,000 | 10.30% |

| Bracket 9 | Over $25,000,000 | 10.90% |

Married couples filing jointly benefit from higher tax bracket thresholds, which helps reduce the so-called “marriage penalty.”

Standard Deduction

New York offers a standard deduction of $8,000 for single filers and $16,050 for married filing jointly. Itemizing can yield greater savings for those with large deductible expenses.

New York City Income Tax

If you live within the five boroughs of New York City, you owe an additional city-level income tax on top of the state tax. NYC’s city tax runs from 3.078% to 3.876% across four income-based brackets.

NYC Tax Brackets

| Filing status (single) | Income range | NYC rate |

| Bracket 1 | $0 – $12,000 | 3.078% |

| Bracket 2 | $12,001 – $25,000 | 3.762% |

| Bracket 3 | $25,001 – $50,000 | 3.819% |

| Bracket 4 | Over $50,000 | 3.876% |

Yonkers residents face a different surcharge, which includes a city income tax of 16.75% of the state tax owed. This effectively adds about 1.1 to 1.8 percentage points to the overall tax rate, depending on income level.

Who Must Pay NYC Tax

Only residents who live within the five boroughs of New York City owe the city income tax. Commuters who work in NYC but live in another state do not owe the city tax.

Combined Tax Burden in New York City

New York City residents have the highest combined income tax burdens in the entire country, before federal taxes are even considered. For a middle-income NYC resident earning $80,000, the combined effective rates across state and city taxes can approach 9–10%. Here’s a simplified look at how those layers compare:

| Tax layer | Rate |

| Federal | ~22% effective |

| NY State | ~5.85% marginal |

| NYC city | 3.876% top |

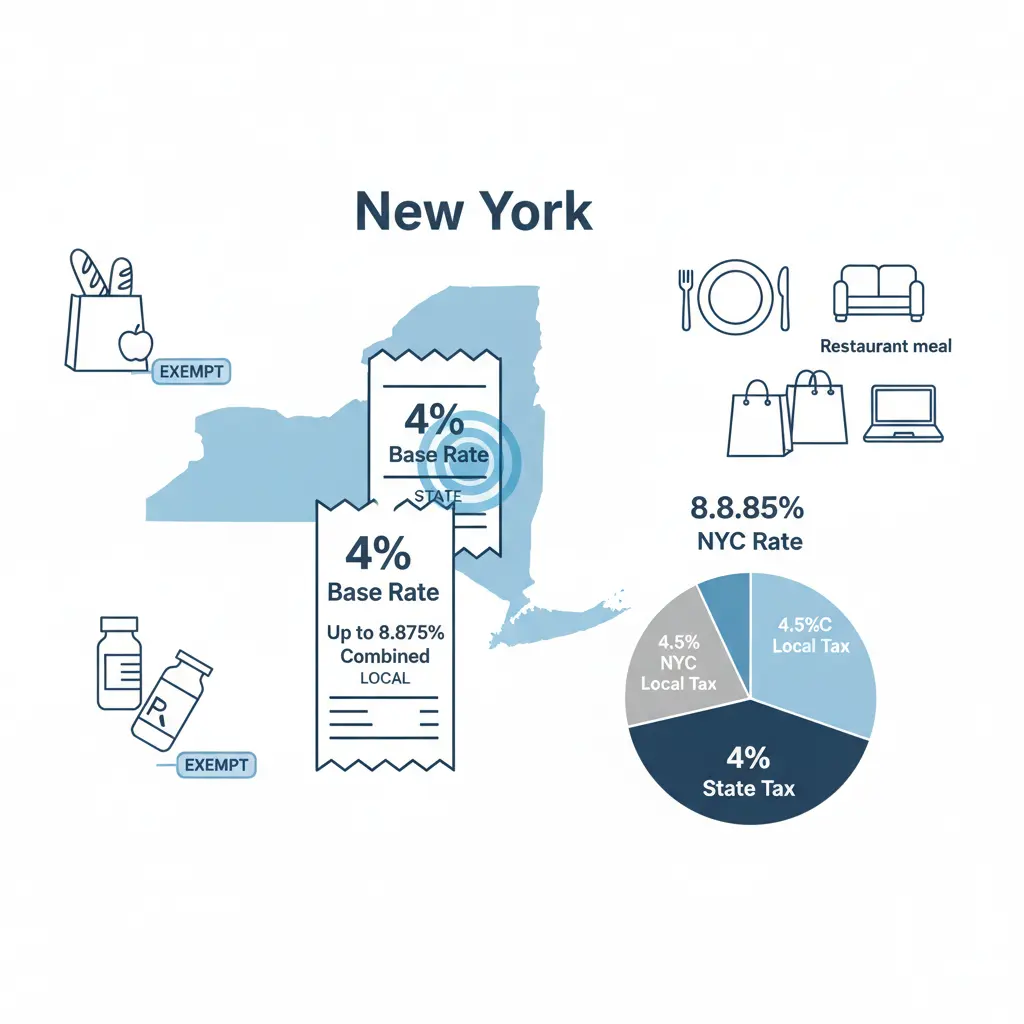

Sales Tax in New York

New York’s base sales tax rate is 4%. However, counties and cities add their own surcharges on top, so the rate most residents actually pay is higher.

Combined State and Local Rates

In New York City, the combined rate is 8.875%, comprising the 4% state rate, a 4.5% city surcharge, and a 0.375% Metropolitan Commuter Transportation District levy. Most counties in the state charge between 7% and 8.75% combined.

Sales Tax Exemptions in New York

Not everything is subject to sales tax. Most groceries (unprepared food) and prescription drugs are not taxable in New York. Clothing items under $110 per item are also not taxable. Prepared food and restaurant meals, electronics, furniture, and luxury goods are fully taxable.

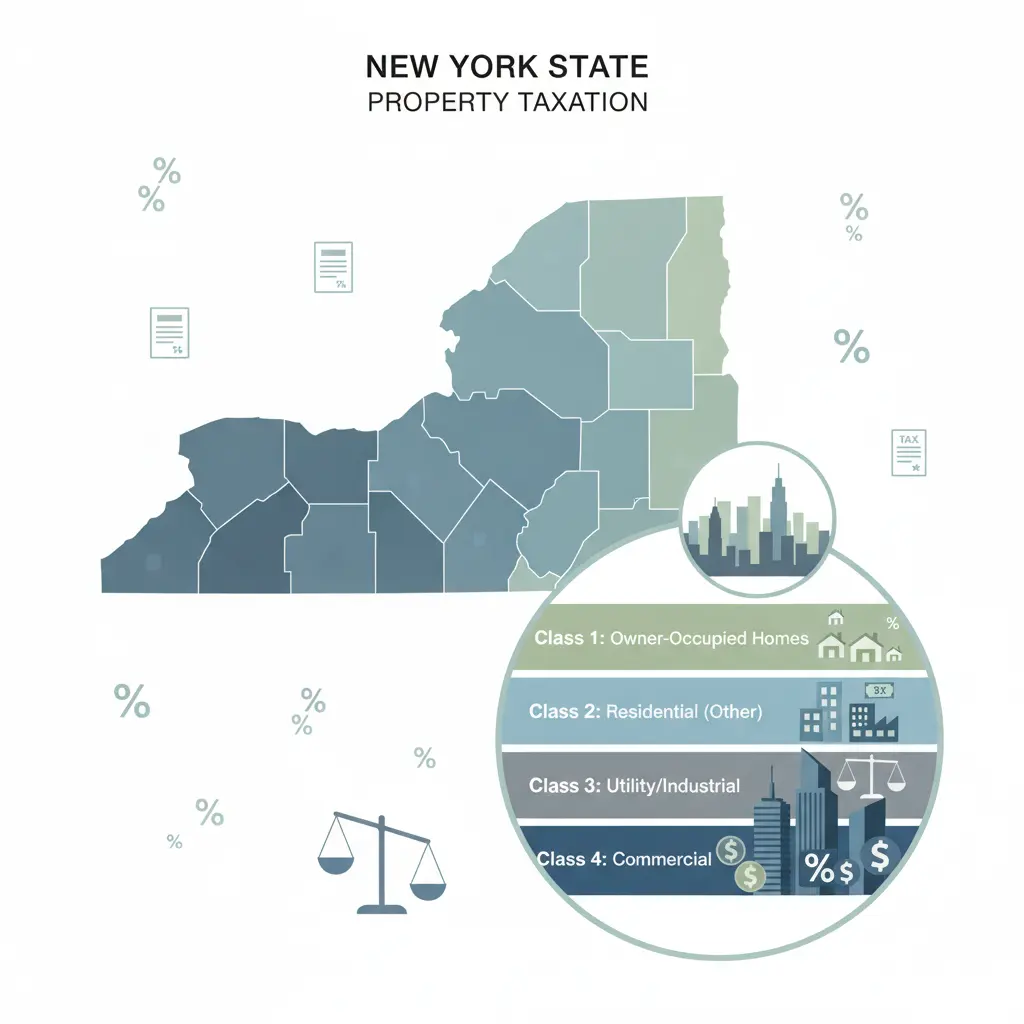

Property Tax in New York

Property taxes in New York are not charged by the state itself. It was charged by local governments, which include counties, cities, towns, and school districts. Rates vary widely across the state.

New York City uses a complex system of four tax classes. For owner-occupied residential properties (Class 1), taxes are significantly lower than for commercial properties. Outside the city, effective property tax rates frequently range from 1.5% to over 3% of assessed value, making some suburban counties among the highest in the nation.

Estate and Capital Gains Taxes

Estate Tax Rates and Exemption

New York is one of a handful of states with their own estate tax, imposed separately from the federal system. The exemption threshold for 2026 is $7.35 million, and rates run from 3.06% to 16% on estates above that threshold.

Estate Tax “Cliff” Rule

New York’s estate tax includes a notable “cliff” provision. So if an estate exceeds the exemption by more than 5%, the entire estate becomes taxable and not just the portion above the exemption. This can result in a dramatically higher tax bill for estates that cross the threshold by even a modest amount. So it needs careful estate planning for high-net-worth individuals.

Capital Gains Tax Treatment

Capital gains in New York are taxed as ordinary income. It means that they are added to your other income and taxed at the same progressive state and city rates. There is no preferential capital gains rate at the state level, unlike the federal system.

Key Tax Rules Residents Often Miss

New York Domicile Rule (183-Day Test)

New York is aggressive about establishing tax residency. If you maintain a permanent place of abode in New York and spend more than 183 days per year in the state, you are taxed as a full resident, even if you claim domicile elsewhere. Documenting days spent outside New York is essential for anyone attempting to establish non-residency.

The SALT Deduction Cap

Federal law caps the state and local tax (SALT) deduction at $40,000. This is a significant limitation for high-income New Yorkers. Which means it prevents them from fully deducting their substantial state and city taxes from federal taxable income. New York’s Pass-Through Entity Tax (PTET) offers some workaround relief for business owners.

Retirement and Pension Tax Rules

New York is relatively retirement-friendly in one respect; first, Social Security benefits are fully exempt from state income tax. Then the Distributions from public pensions, including New York State and local government pensions, are also fully exempt. Private pension distributions can be partially excluded, up to $20,000 per year.

Filing and Payment Deadlines

New York State income tax returns (Form IT-201 for residents) are due April 15. This also aligned with the federal deadline. An automatic extension to October 15 is available, which extends only the filing deadline. Additionally, any taxes owed must still be paid by April 15 to avoid interest and penalties. Estimated quarterly tax payments are required if you expect to owe more than $300 in New York tax for the year.

Conclusion

New York is one of the most layered tax systems in the country. Between the progressive state income tax, the additional city tax for NYC residents, sales and property levies, and the estate tax’s cliff provision, the cumulative burden can be substantial, particularly for higher earners and those living in New York City. That said, the system also provides meaningful relief, such as Social Security and public pension income, which are fully exempt. Additionally, standard deductions reduce taxable income for most filers, and sales tax exemptions on groceries and clothing provide everyday savings. The rules governing residency, domicile, and the SALT deduction cap are where many taxpayers run into unexpected liabilities. Understanding how these interact, especially if you split time between states, own a business, or are approaching retirement, is worth the attention. When in doubt, working with a qualified tax professional familiar with New York law can help you navigate the specifics of your situation and avoid costly surprises. The rules governing residency, domicile, and the SALT deduction cap are where many taxpayers run into unexpected liabilities. Understanding how these interact, especially if you split time between states, own a business, or are approaching retirement, is worth the attention. When in doubt, working with a qualified tax professional familiar with New York law can help you navigate the specifics of your situation and avoid costly surprises. For your tax solution, The Chamberlain Accounting Firm provides a full range of services, including individual tax returns (1040), business returns (1065, 1120, 1120S), and comprehensive bookkeeping solutions, and we specialize in law firm accounting as well. We proudly serve clients throughout Bergen County, New Jersey, and nearby communities, as well as multiple states across the U.S. For personalized guidance and reliable support, reach out to us online or call (201) 371-3344 today.

Disclaimer: This article is provided for general informational purposes only and does not constitute accounting, tax, or financial advice. The information contained herein is not intended to be relied upon for specific tax, accounting, or financial decisions, and may not reflect current tax law or guidance. No opinion expressed herein may be used for the purpose of avoiding penalties under federal, state, or local tax laws. Readers should consult with a qualified accounting or tax professional regarding their specific circumstances. This communication does not create an accountant-client or advisory relationship.